Strategy - option risk app for iPhone and iPad

4.0 (

6080 ratings )

Finance

Education

Developer: Iaroslav Mironov

Free

Current version: 1.0, last update: 6 years agoFirst release : 31 Jan 2018

App size: 7.98 Mb

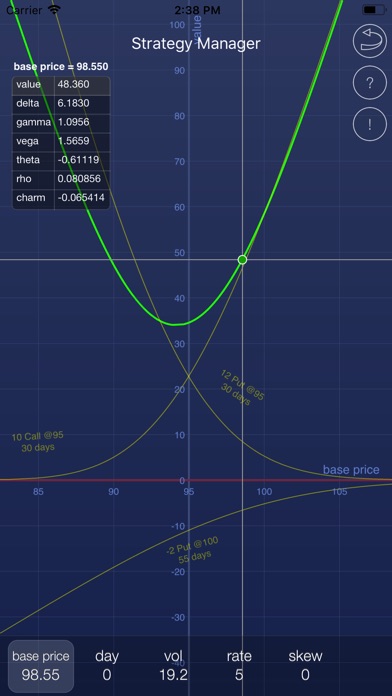

* Study option stategies, spreads, swaps, option models

* Create real-time interactive risk and value graphs

* Create and test your own strategies (via InApp)

You can run simulations for the value of various risk parameters: delta, gamma, vega, theta.

You can study changes to the strategy value as well as to various strategy risk parameters, e.g., you can see how the delta of a strategy will change if market prices drop and volatilities rise. Or how much theta value you can get per one day of holding your position as it approaches expiry.